Explore

Can you believe we’re already halfway through 2025? Q2 is in the books, July is here, and summer’s in full swing!

But don’t expect any slow, sleepy “dog days” in this economy—things are legit getting crazier by the week! Buckle up, because we’ve got another wild (and holiday-shortened) week to break down. Let’s get it!!

We are posting regular content to Instagram (Nick | Kreg) and Facebook (Nick | Kreg) to help you and your buyers stay informed. Be sure to follow us!

Read time: ~4 minutes

Love it or hate it, the "Big Beautiful Bill Act" was officially signed into law on July 4th.

So now that it’s done, what does it actually mean for us in the real estate world? Let’s break down what matters most to us in the industry:

Key Takeaway: The "Big Beautiful Bill" delivers major wins for the real estate industry—keeping the mortgage interest deduction, supercharging tax write-offs for investors, and locking in a bigger, permanent tax deductions. Whether you're an agent, investor, or developer, this bill puts more money in your pocket.

Nick and I have been saying it for a while—and now the data backs it up: a July rate cut isn’t happening.

Trump’s throwing jabs at “Too Late Powell” for keeping rates elevated, while Bill Pulte (U.S. Director of Federal Housing) is calling for a full-blown investigation into Powell for “political bias” and wants him gone.

The Fed is supposed to be neutral… but let’s be honest—inflation was higher and unemployment was the same last September, and we still got a surprise 0.50% cut right before the election. Not the best look for Powell as that doesn’t exactly scream non-partisan.

But politics aside, let’s look at what actually matters: the numbers.

📊 Should the Fed Be Cutting Right Now?

Short answer: Absolutely not.

Rate cuts usually come when the job market shows signs of weakness. But the June Jobs Report landed last Thursday, and it was solid:

These numbers were strong—really strong. And they gave Powell all the ammunition he needed to say, “Nope, we’re not touching rates right now.”

None. Zero. Zilch. Period.

Markets reacted fast after the hot Jobs Report:

With the next Fed meeting on July 30, the odds of a rate cut are sitting at just 4.7%. Translation: not happening.

Trump and Pulte might be losing their ever-loving minds right now, but the bottom line is this: The Fed isn’t cutting rates anytime soon. And the market knows it.

Key Takeaway: The noise is loud, but the data's louder. With a strong June jobs report and unemployment dropping, the chances of a July rate cut are basically dead. Markets have already adjusted, and mortgage rates are trending up as a result. Expect rates to remain higher for longer.

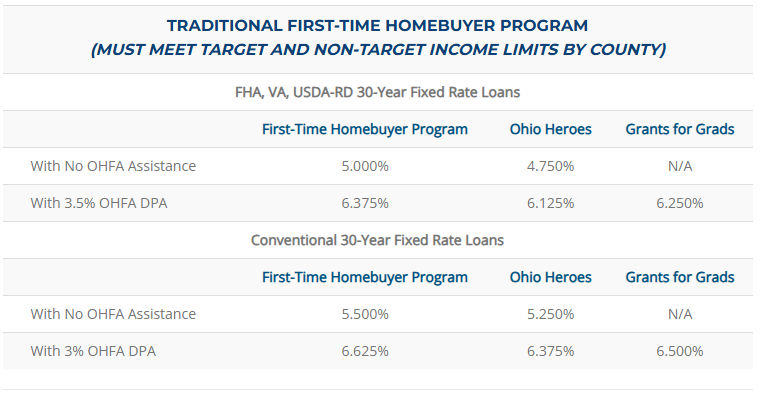

I know some of you are tuning in from outside Ohio—so you can either skip this part… or double down and start marketing the hell out of these new rates to your Ohio clients! Trust me, they’re that good!

Nick took this video of me on my way to the office to tell all my agents about the new OHFA rates:

On Tuesday, July 1st, in a surprise move, the Ohio Housing Finance Agency (OHFA) dropped rates big time:

One client in particular had her eye on a $500,000 home but was on the fence due to the payment at the current market rate of 6.75%. We reran the numbers at the new 5.25% rate:

✅ Monthly payment dropped by $386

✅ Total interest saved over the life of the loan: $138,808

✅ She placed an offer within 24 hours and is now under contract

If this doesn’t show how powerful interest rates are, I don’t know what does. The low 5’s are clearly the sweet spot that unlocks real buyer demand—and OHFA just lit the match.

We’re already seeing more activity, more urgency, and more buyers ready to move.

And we are so here for it!

Key Takeaway: OHFA just dropped rates into the low 5’s, and it’s already igniting serious buyer activity. For eligible Ohio buyers, this means lower monthly payments, huge interest savings, and a real reason to act now. And you don't necessarily have to be a first-time homebuyer! If you’re not marketing this, you’re missing the moment.

Advertised offers are not guaranteed if you do not continue to meet Lower’s criteria and other factors bearing on your creditworthiness. Rates will vary depending on your loan term, loan type, credit profile & score, down payment, qualifying ratios, and property collateral. Monthly payments do not include property taxes, property insurance, and homeowners’ association dues. Since costs can vary based on a loan program, closing costs are not shown in examples. To qualify for a mortgage, borrowers must be U.S. citizens or permanent residents, and meet Lower’s underwriting and Investor requirements. Interest rate examples are as of 03/17/2025. All loans are subject to underwriting or investor approval. Other restrictions may apply. This is not an offer of credit or a commitment to lend. Rate subject to change depending on time of lock.

© 2025 Lower, LLC | NMLS#1124061 | www.nmlsconsumeraccess.com | 2021 Lower Holding Co. Lower is a family of Companies. Conducts business as Lower.com, LLC in 38 States. Arizona, Arkansas, California, Connecticut, Delaware, District of Columbia, Florida, Idaho, Iowa, Kansas, Kentucky, Louisiana, Maine, Massachusetts. Minnesota, Mississippi, Missouri, Montana (Lowerdotcom, LLC), Nebraska, New Hampshire, New Jersey, New Mexico, North Carolina, North Dakota, Ohio, Oklahoma (Lower Mortgage, LLC), Oregon, Pennsylvania, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, Washington, West Virginia, Wisconsin, and Wyoming.